3/15/2018

Loan Rates are going up just as predicted.

The experts (including NCUA examiners) warned us back in 2010 that interest rates were going up. Be prepared they said. It’ll kill your bottom line when it happens. Well finally, they’re right. Rates are steadily going up. The average Auto Loan rate from my sample is 3.22%, as of today. Compare this to 2.89% back in June of 2017. Credit Unions, that are paying attention, are now around 3.5%. I think we’ll soon find everyone at 3.5% or higher. Credit Unions are following the long traditional strategy of raising loan rates quickly, when rates go up, and raising deposit rates much more slowly. (These days they even factor this into most of the ALM models).

Long Term Auto Loans

I noticed just two credit union willing to go 8 and 9 years on an Auto Loan. I know that we’ve all been told how risky this is. And I agree. However, it’s not much more risky than financing a 4 year old auto (and older) for 5 years.

With the current price of high end autos, more members will want to finance their BMW or Pick-Up for 8 or 9 years. I guess Utah First and AFCU will be getting that business.

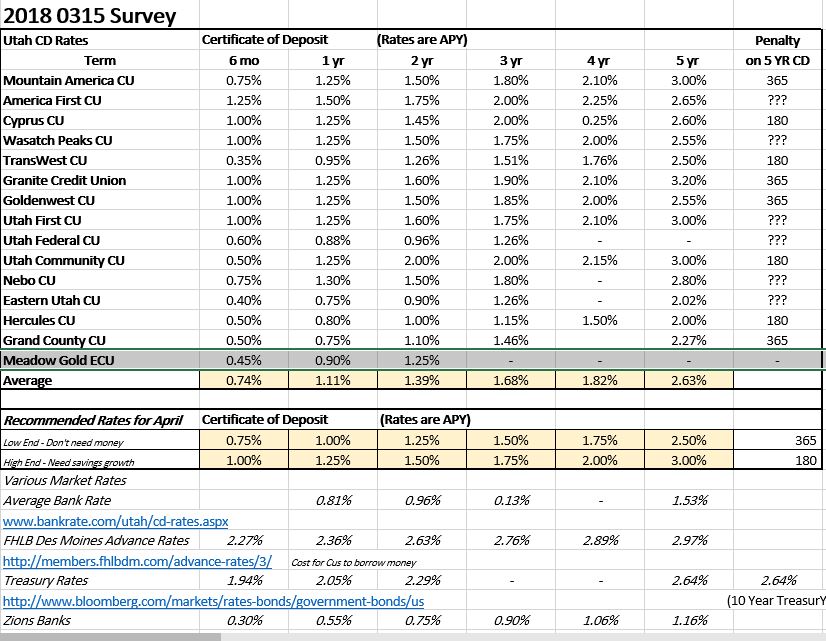

CD Rates are Moving Up

Credit Unions are definitely moving rates up on Certificate of Deposits. Members with CDs pay attention to the market rates and demand higher rates. Plus they shop around so credit unions have responded to these members by raising rates. The average rate on a 5 year CD is now 2.63% (with my sample group). Back in March of 2017 it was 2.17%. An increase of 46 basis points. 1 year CDs increased from .67% to 1.11%. (An increase of 44 basis points). Credit Unions are fairly competitive for 5 year CDs considering that the 10 year treasury is at 2.64%. (The old rule use to be to pay no more than 25 basis points more than the treasury). Paying over 2.6% doesn’t make much sense to me unless you desperately need the deposits.

The scarier rate is the 2 year treasury at 2.29%. With credit unions paying an average of just 1.39% on a 2 year CD, members would be nuts depositing for two years at a credit union when they can earn over 2% in treasuries. There will be a lot of pressure to move rates up on the shorter end.

CD Rates Survey

Regular Savings and Money Market Rates

Why bother posting these rates? No credit union surveyed moved rates on savings and money markets accounts. (Most haven’t move rates in 8 or 9 years). If any moved recently I may have missed it since I got bored looking. These rates will eventually have to come up. It’ll be interesting to see who moves first.

6/27/2017

Auto Loan Rates are Going Up … But Not Everywhere

In June Salt Lake City’s two major players, Mountain America Credit Union and America First Credit Union, raised their auto loan rates. Both are at 3.24% APR for their benchmark 60 month term with A+ credit…and a checking account. Of course, rates are complicated to compare.

However, it seems that most credit unions could raise at least 25 basis points without being pummeled by their members and having everyone run to Mountain America.

If your credit union has a cash-back deal on direct loans there is no need to beat Mountain America’s rate and pay cash back.

When rates go up, slow to raise your savings rate can boost your bottom line. However, to be slow to raise your loan rates can only hurt the bottom line.

Don’t be surprised if there are a number of additional credit unions raising rates on July 1st. A little late as usual.

3/16/2017

Federal Reserve Chairman Announces Fed Funds Increase

On Wednesday, March 15th, Chairman Janet Yellen announced that the central bank’s overnight target rate was raised from .75% to 1%. It appears that the increase in rates that most credit union executives have been predicting for the past 8 years is finally here. The Chairman indicated that we could expect a couple more raises by the end of the year.

So what do you do with your credit union savings rates?

Historically, financial institutions are slow to raise rates on savings in a rising rate environment. Obviously, raising rates quickly cuts into net earnings. On the other hand, raising rates too slowly can create serious liquidity concerns and cost you credibility with your members…as they make withdrawals chasing higher rates.

On the loan side, rates on HELOCs rise with the increases in the Fed Funds rate and the accompanying raise in bank Prime Rates. If you have too much liquidity like many credit unions, go ahead and drag your feet. Raise your rates only after you are way under the market and can’t stand the embarrassment any more. I prefer being on the leading edge of raising rates. You establish credibility with your members and you may experience some fairly strong asset growth…and since the market rates of your investments go up faster than credit unions raise money, you can generally make a nice little spread even on the money you have to invest.

The CD rate survey speaks for itself but let me make a couple of points.

- Credit Unions can borrow for 5 years from the FHBL at 2.42% so why pay much more than that for a 5 year Certificate of Deposit. A 5 year Treasury is at 2.05%. You should pay at least that amount.

- A member could invest in a 6 month treasury bill and get an .87% return. The average CD at a Utah Credit Union is .36%. We’ll soon have to be paying at least .90% for a 6 month CD. But don’t rush.

Raising rates on Shares and Money Market Accounts is especially painful. It has an instant impact on your bottom line. Monitor your deposit balances carefully to determine when you absolutely have to raise your rates. And by the way, it’s time to raise your loan rates. No reason to delay that. Be the first…everyone has to follow.

The Fun

Managing rates is the fun part of your job. Good luck.